Economic Democracy: The Basic Model

This passage is excerpted from After Capitalism by David Schweickart.

The model to be elaborated here and defended in subsequent chapters does not originate simply from economic theory, nor is it a stylized economic structure of some particular country or region. The model is a synthesis of theory and practice. What I call “Economic Democracy” is a model whose form has been shaped by the theoretical debates that have taken place over the past thirty years concerning comparative economic systems, by the empirical studies of modes of workplace organization, and by the records of various historical “experiments” of the twentieth century, notably the Soviet Union, postwar Japan, Tito’s Yugoslavia, China after Mao, and (smaller in scale, but extremely important) a most unusual “cooperative corporation” in the Basque region of Spain.

The model also derives from an analysis of two sources of felt discontent with capitalism, discontent already acute in many quarters and likely to intensify. (It is precisely this discontent that gives the model a practical dimension. If people are basically content with the way things are, alternatives, even if superior, are of theoretical interest only.) Both sources of discontent may be regarded as “democratic deficits”—lack of democratic control over conditions that affect us deeply.

The first concerns workplace democracy. It is a striking anomaly of modern capitalist societies that ordinary people are deemed competent enough to select their political leaders—but not their bosses. Contemporary capitalism celebrates democracy, yet denies us our democratic rights at precisely the point where they might be utilized most immediately and concretely: at the place where we spend most of the active and alert hours of our adult lives. Of course, if it could be demonstrated that workplace democracy is too cumbersome to be efficient or workers too ignorant or shortsighted to make rational decisions, this would be a powerful counterargument to extending democracy in so logical a direction. But, as we shall see, the evidence points overwhelmingly to the opposite conclusion: workplace democracy works—in fact, as a general rule, workplace democracy works better than owner-authoritarianism, that is, the capitalist form of workplace organization.

The other disconcerting feature of contemporary capitalism is capital’s current “hypermobility.” The bulk of capital in a capitalist society belongs to private individuals. Because it is theirs, they can do with it whatever they want. They can invest it anywhere and in anything they choose, or not invest it at all if profit prospects are dim. But this freedom, when coupled with recently enhanced technical transfer capabilities, gives capital a mobility that now generates economic and political insecurity around the globe. Financial markets now rule, however “democratic” political systems purport to be, and this rule is often capricious, often destructive.

Let us consider a socialist alternative to capitalism that addresses these democratic deficits. It’s socialism quite different in structure from the failed models of the past. (I use the term “socialist” to refer to any attempt to transcend capitalism by abolishing most private ownership of means of production. Although differing in other ways from earlier attempts to get beyond capitalism, Economic Democracy shares with them the conviction that private ownership of the means of production must be curtailed if the human species is to flourish.)

Economic Democracy, like capitalism, can be defined in terms of three basic features, the second of which it shares with capitalism:

• Worker self-management: Each productive enterprise is controlled democratically by its workers.

• The market: These enterprises interact with one another and with consumers in an environment largely free of governmental price controls. Raw materials, instruments of production, and consumer goods are all bought and sold at prices largely determined by the forces of supply and demand.

• Social control of investment: Funds for new investment are generated by a capital assets tax and are returned to the economy through a network of public investment banks.

This basic model, which will be elaborated more fully below, is necessarily stylized and oversimplified. In practice, Economic Democracy will be more complicated and less “pure” than the version presented here. However, to grasp the nature of the system and to understand its essential dynamic, it is important to have a clear picture of the basic structure. (The same is true of capitalism. Economists generally use simplified models to explain the basic laws of the system.)

Recall that capitalism is characterized by private ownership of means of production, the market, and wage labor. The Soviet economic model abolished private ownership of the means of production (by collectivizing all farms and factories) and the market (by instituting central planning) but retained wage labor. Economic Democracy abolishes private ownership of the means of production and wage labor, but retains the market.

Worker Self-Management

Each productive enterprise is controlled by those who work there. Workers are responsible for the operation of the facility: organization of the workplace, enterprise discipline, techniques of production, what and how much to produce, what to charge for what is produced, and how the net proceeds are to be distributed. Enterprises are not required to distribute the proceeds equally. In all likelihood, most firms will award larger shares to more highly skilled workers, to those with greater seniority, and to those with more managerial responsibility. Decisions concerning these matters will be made democratically. (Disgruntled members are free to quit and seek work elsewhere, so egalitarian considerations must be balanced against the need to motivate and retain good workers.)

In a firm of significant size, some delegation of authority will be necessary. The usual solution to this general problem of democracy is representation. Most enterprises will have an elected workers’ council that will appoint a general manager or chief executive officer and perhaps other members of upper management. Management is not appointed by the state or elected by the community at large or, since this is not a capitalist corporation, selected by a board of directors elected by stockholders. (There are no stockholders in Economic Democracy.)

An important practical issue emerges at this level—getting the right balance between managerial accountability and managerial autonomy. Accountability without autonomy risks timidity and paralysis; autonomy without accountability risks despotism. Managers need sufficient autonomy so that they can manage effectively, but not so much that they can exploit the workforce to their own advantage. It can be assumed that various enterprises will handle this issue differently, the more successful models being emulated. (As we shall see, highly successful models already exist.) Whatever internal structures are put in place, ultimate authority rests with the enterprise’s workers, one-person, one-vote.

Although workers control the workplace, they do not “own” the means of production. These are regarded as the collective property of the society. Workers have the right to run the enterprise, to use its capital assets as they see fit, and to distribute among themselves the whole of the net profit from production. Societal “ownership” of the enterprise manifests itself in two ways.

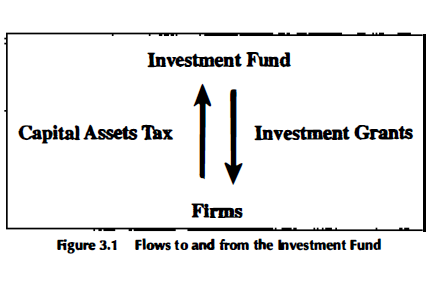

• All firms must pay a tax on their capital assets, which goes into society’s investment fund. In effect, workers rent their capital assets from society. (More on this below.)

• Firms are required to preserve the value of the capital stock entrusted to them. This means that a depreciation fund must be maintained. Money must be set aside to repair or replace existing capital stock. This money may be spent on whatever capital replacements or improvements the firm deems fit, but it may not be used to supplement workers’ incomes.

If an enterprise finds itself in economic difficulty, workers are free to reorganize the facility or to leave and seek work elsewhere. They are not free to sell off their capital stocks and use the proceeds as income. A firm can sell off capital stocks and use the proceeds to buy additional capital goods. Or, if the firm wishes to contract its capital base so as to reduce its tax and depreciation obligations, it can sell off some of its assets; in this case, proceeds from the sale go into the national investment fund, not to the workers, since these assets belong to society as a whole. If a firm is unable to generate even the nationally specified minimum per capita income—Economic Democracy’s equivalent to the minimum wage—then it must declare bankruptcy. Movable capital will be sold to pay creditors. Its workers must seek employment elsewhere.

In essence, a firm under Economic Democracy is regarded not as a thing to be bought or sold (as it is under capitalism) but as a community. When you join a firm, you receive the rights of full citizenship; you are granted an equal voice, namely, an equal vote in the community. When you leave one firm and join another, these rights transfer. With rights come responsibilities, in this case the responsibilities of paying the capital assets tax and maintaining the value of the assets you are using.

The Market

Economic Democracy is a market economy, at least insofar as the allocation of consumer and capital goods is concerned. Firms buy raw materials and machinery from other firms and sell their products to other enterprises or consumers. Prices are largely unregulated except by supply and demand, although in some cases price controls or price supports might be in order—as they are deemed in order in most real-world forms of capitalism.

Since enterprises in our economy buy and sell on the market, they strive to make a profit. (“Profit” is not a dirty word in this form of socialism.) However, the “profit” in a worker-run firm is not the same as capitalist profit; it is calculated differently. Market economy firms, whether capitalist or worker self-managed, strive to maximize the difference between total sales and total costs. However, for a capitalist firm, labor is counted as a cost; for a worker-run enterprise, it is not. In Economic Democracy, labor is not another “factor of production” on technical par with land and capital. Instead, labor is the residual claimant. Workers get all that remains, once non-labor costs, including depreciation set-asides and the capital assets tax, have been paid. (As we shall see, this seemingly small structural difference will have far-reaching consequences.)

“Market socialism” remains a controversial topic among socialists. I and many others have long argued that centralized planning, the most commonly advocated socialist alternative to market allocation, is inherently flawed, and that schemes for decentralized, nonmarket planning are unworkable. Central planning, as theory predicts and the historical record confirms, is both inefficient and conducive to an authoritarian concentration of power. This is one of the great lessons to be drawn from the Soviet experience. I won’t pursue the argument here. I will simply assert what I take to be a growing consensus even among socialists: Without a price mechanism sensitive to supply and demand, it is extremely difficult for a producer or planner to know what and how much to produce, and which production and marketing methods are the most efficient. It is also extremely difficult in the absence of a market to design a set of incentives that will motivate producers to be both efficient and innovative. Market competition resolves these problems (to a significant if incomplete degree) in a non-authoritarian, non-bureaucratic fashion. This is an achievement indispensable to a serious socialism.

Social Control of Investment

This is the most technically complex feature of our model. It is vastly simpler than the institutions that comprise the investment mechanisms of capitalism (i.e., those mysterious, omnipotent “financial markets”) but it is more complicated to specify than is worker self-management or the market.

In any society that wants to remain technologically and economically dynamic, a certain portion of society’s labor and natural resources must be devoted each year to developing and implementing new technologies and to expanding the production of the goods and services in high demand. In a modern society, this allocation of resources is effected through monetary investment. From where do investment funds come? In a capitalist society, they come largely from private savings, either the direct savings of private individuals or the retained earnings of corporations, that is, the indirect savings of stockholders. These savings are then either invested directly, or deposited in banks or other financial institutions, which lend them out to businesses or entrepreneurs.

In Economic Democracy, investment funds are generated in a more direct and transparent fashion. We simply tax the capital assets of enterprises—land, buildings, and equipment. This tax, a flat rate tax, may be regarded as a leasing fee paid by the workers of the enterprise for use of social property that belongs to all.

Receipts from the capital assets tax constitute the national investment fund, all of which is earmarked for new investment. (“New investment” is simply investment over and above that financed by enterprises directly from their own depreciation funds.) All new investment derives from this fund. In stark contrast to capitalism, Economic Democracy does not depend on private savings for its economic development.

Since investment funds are publicly, not privately, generated, their allocation back into the economy is a public, not a private, matter. Society must decide on procedures that are both fair and efficient. Here we have options. Not surprisingly, there’s no set of procedures that can guarantee perfect efficiency and perfect fairness, but there do exist various mechanisms that can be employed to produce more rational, equitable, and democratic development than can be expected under capitalism.

At one extreme, a democratically accountable planning board could allocate all the funds according to a detailed plan. This would not be a plan for the entire economy, a la Soviet central planning, but only for new investments (in a country like the United States, roughly 10 to 15 percent of GDP), so it would not run up against the insurmountable difficulties inherent in the Soviet model. Such planning would be more akin to that practiced by Japan and South Korea during their periods of most rapid development—“market conforming” investment planning. For a country in which developmental priorities are relatively clear and widely accepted, such planning might be appropriate.

At the other extreme, these funds could simply be distributed to a network of public banks that would then lend them out using precisely the same criteria that capitalist banks would use. This would be a kind of laissez-faire socialism: let the market decide investment allocation. Banks would be charged a centrally determined interest rate on the funds they receive. They would be expected to make a profit, that is, to charge more than the base-rate interest, adjusted according to risk. Bank officials, who are public officials, would be paid in accordance with performance. Banks would compete, as they do now, trying to balance the riskiness of their loans against the interest rates they charge. As under capitalism, managers of successful banks (i.e., the most profitable) would be rewarded, managers whose banks performed poorly would be sacked. In all cases, bank profits are returned to the national investment fund.

In my view, the optimal mechanism, at least for a rich country, lies between these extremes. Decision-making is far more decentralized than in the first alternative; the market is more constrained than in the second. Concerns for justice and efficiency are balanced by using a mix of market and nonmarket criteria. The basic idea is to allocate the centrally collected funds according to a principle of fairness first, and then to bring in competition to promote efficiency. Efficiency will be understood to include not only technical efficiency, but “Keynesian efficiency” as well, that is, full employment. (In the Keynesian view, it is not efficient to have able-bodied people unemployed. That’s a waste of a valuable resource.)

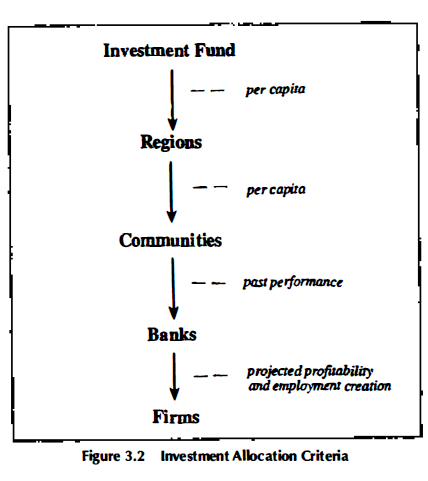

The principle of fairness pertains to regional and communal distribution: each region of the country and each community within each region is entitled to its fair share of the national investment fund. “Fair share” is understood to be, prima facie, its per capita share; that is to say, if Region A has X percent of the nation’s population, it gets X percent of the money available for new investment. The central implication of this principle is that regions and communities do not compete for investment funds. They do not compete, as they must under capitalism, for capital. Each region and each community gets its share, each and every year, as a matter of right.

Two ethical-sociological assumptions serve to ground this “fair share” requirement:

• Societal health requires that individuals develop intergenerational commitments and a sense of place, these being facilitated by regional and community stability.

• Although individuals should be free to move to other regions or communities if they so desire, they should not be compelled to do so—not even if there is some marginal gain in overall economic efficiency if society’s labor force is reallocated.

Guaranteeing each region and each community a steady supply of investment funds each year mitigates the coercion that a purely market-determined allocation of investment funds is likely to produce. Since this guarantee enhances regional and community stability without encroaching on an individual’s freedom, it should be part of the investment-allocation mechanism. (If large efficiency gains can be had by pressuring people to relocate, then the argument for per capita allocation of investment funds is less compelling—although the case would have to be made that the efficiency gains are sufficient to offset the real costs of labor migrations. In a truly democratic society, investment allocations would be subject to democratic control. Market allocation would not be presumed “natural,” nor would efficiency concerns automatically trump all others.)

Why should “fair share” be per capita share? We observe that it would not be fair simply to return to each region the investment funds collected (via the capital assets tax) from that region, since that amount merely reflects the quantity of capital assets in that region. The fact that one region has a larger capital base than another is not due to the greater effort expended by the people in that region, or to their greater intelligence or moral worth, but to the region’s specific history. It would hardly be fair to base present capital allocation on past history. Doing so would give a disproportionate share to the regions that are already more capital intensive, thus exacerbating, rather than mitigating, regional inequalities.

This, of course, is precisely what happens under capitalism. (Real-world capitalism, that is, as opposed to neoclassical fiction, where capital always flows from areas of greater capital intensity to those of lesser.) New investment tends to flow to where the capital base is already large. Cities attract more capital than rural areas. Industrial centers suck investment funds from the rest of a country. Capital tends to move to where capital is already plentiful, because that is where new investment opportunities are easiest to find. Workers must then follow, migrating to where new jobs are being created. To be sure, there are counter-movements. An industrial region may decline if shifting patterns of demand or new technologies adversely affect the market for the products being produced there, or if labor unions get too strong, or if social or infrastructure problems make a desirable region less desirable. But this simply means that capital will flow elsewhere, and workers must, if they can, chase after it. (What happens at the national level also happens globally. Rich countries attract more capital than poor countries. Immigration patterns follow suit. Here, we are concerned with developing principles for allocating capital within a given country. Those principles and mechanisms for dealing with inequalities among nations will be discussed later.)

It is clear that the pattern of industrialization and capital density that an Economic Democracy has inherited from its capitalist past cannot be regarded as entitling a capital-intensive region to even more capital. Moreover, if we think about how the market works, we see that capital-intensive regions are not being unfairly disadvantaged by a per capita allocation. The capital access tax is, in fact, a cost of production, and hence covered by the market price of the goods being produced. That is to say, firms in a given industry are all subject to the same tax burden, and so they can (and will) set their prices to cover these taxes. They will not be disadvantaged competitively by doing so. Unfortunately, this perfectly legitimate price setting gives rise to a market illusion. Capital-intensive regions may think they are paying more than their “fair share” of taxes, since they get back less than they pay. What they don’t realize—unless this point is made explicit—is that the market allows their capital-intensive firms to charge more for their products than they would otherwise be able to, precisely to cover these taxes. Ultimately, it is the consumers of the goods, not the firms themselves or the regions in which the firms are located, who pay these taxes; the regions, therefore, have no grounds for complaint.

If one wants a positive justification for the principle of per capita capital allocation, one can appeal to Marx’s insight that labor, not capital, is the source of value, and hence of the surplus value that constitutes the investment fund. If this is so, then the investment fund ought to be distributed to regions in proportion to the size of their workforces, that is, (essentially) on a per capita basis. Or, if one prefers a non-Marxian justification, allocating investment funds to regions may be regarded as providing a public service. Hence, the allocation of investment funds should follow the principle used in the allocation of such public services as education and health care (at least in those parts of the world where education and health care are publicly funded and rationally distributed)—namely, per capita share.

These justifications do not give the per capita principle absolute force. The right of a region or community to its per capita share of the investment fund is a prima facie right only, which can be overridden by other ethical or economic considerations. The modernization of an outmoded industry in a particular region might require that it receive more than its per capita share for a period of time. It might be desirable to allocate a larger than per capita share to an underdeveloped region or community for a number of years, to aid it in catching up. These decisions will have to be made publicly, by the democratically elected national or regional legislature, with full weight being given to the fact that if some regions get more than their per capita share, others will get less.

The principle of fair share governs the allocation of the national investment fund to regions and communities. When this share reaches a community, it is then distributed to public banks within the communities. These banks will make the funds available to local enterprises wanting to expand production, introduce new products, enter new lines of business, upgrade technologies—anything requiring capital in excess of what has accumulated in their depreciation funds.

Banks make grants, not loans, to business enterprises. These grants, however, do not represent “free money,” since an investment grant counts as an addition to the capital assets of the enterprise, upon which the capital asset tax must be paid. Thus, the capital assets tax functions as an interest rate. A bank grant is essentially a loan requiring interest payments but no repayment of principal.

Each bank receives a share of the investment fund allocated to the community, but this allocation is no longer governed by the principle of fair share. A bank’s share is determined by the size and number of firms serviced by the bank, by the bank’s prior success at making economically sound grants, and by its success in creating new employment. (The importance of this third criterion will become clear later.) The bank’s own income, to be distributed among its workforce, comes from general tax revenues (since these are public employees) according to a formula linking income to the bank’s success in making profit-enhancing grants and creating employment. Unlike banks under capitalism, these banks are not themselves private, profit-making institutions. They are public institutions charged with effectively allocating the funds entrusted to them in accordance with two criteria: profitability and employment creation. (A community could impose additional criteria to better control the pattern of development in the community. For the sake of simplicity, I will restrict the nonmarket criterion to the most essential, employment creation.)

If a community is unable to find sufficient investment opportunities to absorb the funds allocated to it, the excess must be returned to the center, to be reallocated to where investment funds are more in demand. This being the case, communities have a strong incentive to seek out new investment opportunities in order to keep the allocated funds at home. Banks also have a similar incentive, so it is reasonable to expect that communities and their banks will set up entrepreneurial divisions—agencies that monitor new business opportunities, and provide technical and financial expertise to existing firms seeking new opportunities and to individuals interested in starting new worker self-managed enterprises. These agencies might go so far as to recruit prospective managers and workers for new enterprises. (As we shall see, the bank at the center of the world’s most successful cooperative experiment, Mondragon’s Caja Laboral Popular, did exactly that—with impressive results.)

One further element of the investment mechanism needs to be considered. In a market economy, two kinds of capital investment take place: “public” investment related to the provision of free (or heavily subsidized) goods and services (e.g., roads, bridges, harbors, airports, schools, hospitals, basic research facilities, and the like) and “private” investment related to goods and services to be sold competitively on the market. Under capitalism, these funds are separately generated: public investment is financed from general tax revenues; private investment comes from private savings. (The separation is not so clean in practice. Governments turn to the private financial markets to finance budget deficits. They also use public money—often large amounts—to subsidize favored private industries.) Under Economic Democracy, all capital investment comes from the same source, namely, the capital assets tax. Thus, key decisions must be made at each level of government as to how much of the investment fund should be allocated for public capital investment, for what, and how much should be left for the market sector. (Note: “capital investment” is investment in durable physical assets. Thus, funds for school construction would come from the investment fund whereas salaries of teachers and operating expenses come from general tax revenues. Similarly, in the “private” [i.e., “cooperative”] sector, funds for new plant construction would come from the investment fund whereas worker incomes and operating expenses come from profits.)

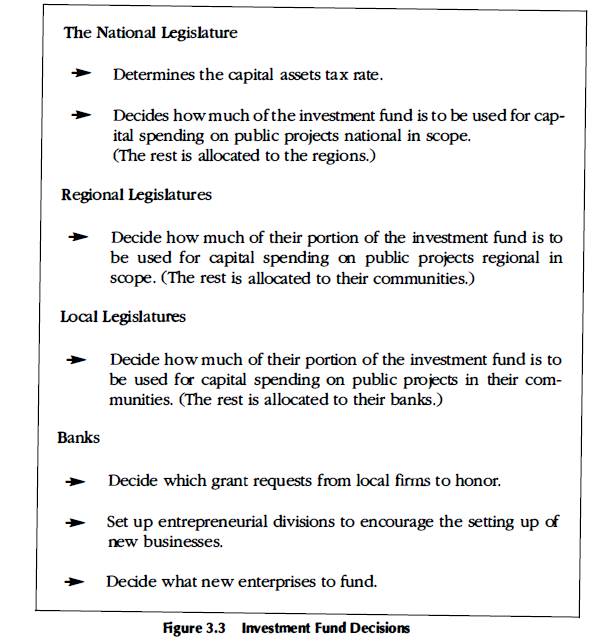

Decisions as to the allocation of investment between the public and market sectors should be made democratically by the legislative bodies at each level, national, regional, and local. Investment hearings should be held, as budget hearings are currently held; expert and popular testimony should be sought. The legislature then decides the nature and amount of capital spending on public goods appropriate to its level, sets these funds aside, then passes the remainder to the next level down.

For example, the national legislature decides, in accordance with the democratic procedures just described, on public capital spending for projects that are national in scope (e.g., an upgrading of rail transport) and then transfers funds to the appropriate governmental agency (e.g., the Department of Transportation). The remainder of the national investment fund is distributed to regions on a per capita basis. Regional legislatures now make similar decisions concerning regional capital spending, then pass the remainder of their investment funds to local communities on a per capita basis. The communities, in turn, make decisions about local public investment, then allocate the remainder to their banks, which make them available to local enterprises. (It should be noted that there is considerable countervailing power in the system to prevent “excessive” public spending—most immediately, all those workers in the enterprises that might want to apply for bank funding, and more generally, the entire citizenry of a community, since everyone knows that a thriving community requires thriving local businesses. Democratically accountable legislative bodies must weigh the benefits to their constituents of more public spending against the need for market sector development. There would seem to be no systematic bias here one way or the other.)

We now have before us the basic structure of “social control of investment.” To summarize: A flat-rate tax on the capital assets of all productive enterprises is collected by the central government, then plowed back into the economy, assisting those firms needing funds for purposes of productive investment. These funds are dispersed throughout society, first to regions and communities on a per capita basis, then to public banks in accordance with past performance, then to those firms with profitable project proposals. Profitable projects that promise increased employment are favored over those that do not. At each level, national, regional, and local, legislatures decide what portion of the investment fund coming to them is to be set aside for public capital expenditures, then send down the remainder, no strings attached, to the next lower level. Associated with most banks are entrepreneurial divisions, which promote firm expansion and new firm creation. Figures 3.1, 3.2, and 3.3 offer a schematic presentation of this summary.

A final observation: The simplified schema just presented has only local banks making grants to local enterprises. Large enterprises that operate regionally or nationally might need access to additional capital, in which case it would be appropriate for the network of local investment banks to be supplemented by regional and national investment banks. These would also be public institutions that receive their funds from the national investment fund.

{kind=link}

{kind=link}

{kind=link}

A Note on the Public Sector

This book concentrates on one part of the economic structure of a viable socialism—those institutions that allocate investment funds and those that utilize such funds to produce goods and services for sale in a competitive market. In chapters 4 and 5, I compare them in their consequences to capitalist institutions and defend their superiority. Very little is said during any of these discussions about those goods and services that will be provided to the citizenry outside the market, notably, child care, education, health care, care for the disabled and care for the elderly. Although the socialist tradition has long insisted that such amenities be offered to all citizens on the basis of need, not ability to pay, the provision of such services, free or at nominal charge, no longer serves to distinguish socialism from capitalism, since many, although certainly not all, advanced capitalist societies do just that. (In almost all cases, such services were introduced under pressure from strong labor movements to head off their more radical demands. Social democratic reforms are not “natural” to capitalism. Not surprisingly, now that globalization has substantially weakened organized labor, efforts are underway everywhere to cut back on public social services.)

I will not offer a detailed specification of the public sector institutions that would be present in any real-world instantiation of Economic Democracy. Economic Democracy will have learned from the experiences of those capitalist countries that have been most successful in providing their citizens with universal health care, quality child care, free education, decent retirement benefits, and the like, and will adopt, perhaps with slight modification, their programs.

Since human solidarity is perhaps the most fundamental of socialist principles, we can expect Economic Democracy to embrace the principle of intergenerational solidarity. This may be understood as follows: A citizen regards all the children of his society as being, in an important sense, his own children, and all the elderly as being his parents. (Philosophers will hear an echo from Plato�s Republic here.) It is reasonable to think in such terms, for, in point of fact, each person born into a humane society is cared for and educated by many members of the older generation, not simply her biological parents, and each must be cared for by members of the younger generation when her generation retires from the labor force. To be sure, biological or other legally recognized parents of children have special rights and responsibilities regarding their biological or adopted children, as do children regarding their legal parents, but it remains the responsibility of each citizen to see to it that no child or older person is neglected.

Regarding children, this principle implies, minimally, that:

- Prenatal and child-rearing classes be made available, free of charge, to all parents.

- Quality day care be available, free of charge, to all parents who require such assistance. (For parents who choose to remove themselves from the paid workforce to care for their children at home, a child care tax rebate might be in order. One mechanism that might be employed: all parents of pre-school-aged children receive “vouchers”—government-issued certificates denominated in dollars—which can be used to pay for certified day care, or, if not used for that purpose, applied to the family�s tax obligations.)

- All children have free access to quality primary and secondary education. (Note: Socialist principles do not preclude providing parents with vouchers to be used at “private” schools. There are two basic rationales for private education. It is sometimes maintained that competition among schools enhances the quality of education. I doubt that this is true, but if a community wishes to try the experiment, it should be free to do so. Market socialism is not opposed to competition. The second rationale concerns religious education. If a society�s constitution prohibits the teaching of religion in public schools, it seems not unreasonable to provide those parents who wish to send their children to religious schools with tuition vouchers. There is nothing “antisocialist” about providing free education for all our children.)

Regarding care for the elderly, the principle of intergenerational solidarity points to a “pay as you go” social security system. That is to say, younger people currently working should pay, via their income or consumption taxes, what is required to maintain in dignity those who can no longer work, or who, even if able, have worked long enough and have chosen to retire. That is to say, everyone in society should come under a public pension plan that is funded by general tax revenues.

“Pay as you go” is usually contrasted with systems in which workers, during their productive years, set aside a portion of their paychecks via mandatory social security deductions and/or voluntary contributions to their pension funds so that, when they retire, they can take care of themselves. In a fundamental sense, this distinction is illusory. If we think in terms of material resources, it is clear that all social security systems are “pay as you go,” because, however pensions and annuities are structured, the material fact is, people who are currently working must produce the goods and services consumed by those who no longer work. It is more honest—and ultimately fairer—for the older generation to acknowledge frankly their dependency on the younger generation than to pretend to be independent—just as that younger generations should acknowledge the fact that their current independence (such as it is) was made possible by an older generation that cared for them for the first two decades or so of their lives.

Economic Democracy: The Expanded Model

A genuine “right to work” has long been a basic tenet of socialism. Every able-bodied person who wants to work should be able to find decent employment. As we shall see in chapter 4, a capitalist economy cannot, for structural reasons, be a full-employment economy. The basic structures of Economic Democracy do not preclude full employment—but they don�t guarantee it either. Hence the need for a supplementary institution that ensures this basic socialist right.

It would be useful to add two more components to the basic, simplified model, components currently existing under capitalism. These institutions may not be necessary to a well-functioning economy, but the citizens of the country might want to retain them anyway, perhaps because they enhance the scope of individual choice and or provide some additional economic benefits. Properly structured, these institutions will not conflict with the basic structure of Economic Democracy or undermine the ethical principles that underlie the system.

Our “expanded model” of Economic Democracy adds three components to the basic model:

- The government as employer-of-last-resort

- Cooperative savings-and-loan associations

- Some private ownership of means of production and some legalized wage labor—that is, some capitalism under socialism

The Government as Employer-of-Last-Resort

Involuntary unemployment is deeply destructive to a person�s sense of self-worth and self-respect. If you are alive, other people have worked, and are working, for you. Other people are growing the food you eat, making the clothes you wear, have built the dwelling in which you reside (even if it is only a homeless shelter). Other people are working for you, but you are giving nothing back. If you search for but cannot find employment, society is in effect saying to you, “There is nothing you can do that we want or need. We may, out of compassion, deign to keep you alive, but you are in fact a parasite, living off the labor of others, contributing nothing in return.” Is it any wonder that prolonged unemployment breeds social pathologies?

A decent society will see to it that every adult who wants to work can have a job. Citizens will have a genuine “right to work.” In Economic Democracy the government will serve as an employer-of-last-resort. It will guarantee a meaningful job to anyone able and willing to work. These jobs will pay an established minimum wage. They will be funded by the central government, but the jobs themselves will be created mostly by regional and local governments in accordance with local needs. Examples of such possible jobs: elder care, child care, playground supervision, caring for parks and other public spaces, nonhazardous environmental cleanup, and low-tech improvement of energy efficiency. On-the-job training will be provided.

Socialist Savings and Loan Associations

In principle, the payment of interest can be abolished under Economic Democracy. Since the economy no longer relies on private savings to generate investment capital, it has no need for the mechanisms that have developed under capitalism to encourage private savings. The economy can function quite well without any private savings at all.

Individuals may still save, but the well-being of the economy as a whole no longer depends on their doing so. Their own individual well-being does not depend on personal savings either. In keeping with the basic principle of intergenerational solidarity, a publicly funded social security system provides all retired persons with decent incomes. People may still want to save, but they don�t have to. In any event, they don�t need to be paid interest on their savings.

However, instead of eliminating interest altogether, it would not be unreasonable for an Economic Democracy to allow a network of profit-oriented, cooperative savings and loan associations to develop. They would function to provide consumer credit, not business credit. If a person wants to purchase a high-cost item for which she does not have ready cash, she can take out a loan from a cooperative S&L to be repaid over time with interest. Money for this loan would come from private savers who, just as under capitalism, would not only enjoy the convenience of having their savings protected, but would also receive interest on their savings (at a somewhat lower rate than what borrowers pay). Housing loans (mortgages) would likely play the dominant role in this sector—as they did in the savings and loan sector in the United States prior to the disastrous deregulation that ushered in the S&L crisis of the late 1980s.

Such S&Ls do not conflict with the values or institutions of Economic Democracy, nor do they pose a threat to economic stability—as do capitalist financial markets. (More on the stability question in chapter 5.) What should not be done is what capitalism does: merge the institutions that generate and distribute investment funds with the institutions that handle consumer credit. Business investment, as opposed to consumer credit, is too important to the overall health of the economy to be left to the vagaries of the market.

Capitalists under Socialism

Would capitalist acts among consenting adults be prohibited under Economic Democracy? This taunting question raised by libertarian philosopher Robert Nozick deserves a response. It should be clear from what has been presented thus far that two of the traditional functions of the capitalist can be readily assumed by other institutions. We don�t need capitalists to select the management of an enterprise (workers are quite capable of doing that), and we don�t need capitalists to provide capital for business investment (such funds can be readily generated by taxation).

There remains the entrepreneurial function. As we observed in chapter 2, the class of entrepreneurs is by no means coextensive with the class of capitalists. Most of the income that flows to holders of stocks, bonds, and other income-entitling securities has no connection whatsoever with productive entrepreneurial activity on the part of the holders of those securities. However, it cannot be denied that some capitalists are entrepreneurs, and that some of the creative innovations such people have produced have been highly beneficial for society. Might it not be desirable to allow a sector of genuinely entrepreneurial capitalism to function under Economic Democracy?

In fact, some capitalism would be permitted in any realistic version of Economic Democracy—or at least some wage labor. The complete abolition of wage labor would require that all enterprises be run democratically, one-person, one-vote. In practice, such a rule would be too rigid. Small businesses need not be run democratically. If the owners of these businesses, who in most cases aren�t true capitalists (since they also have to work), can persuade people to work for them for a wage, there is no need to prohibit such arrangements. The mere fact that most enterprises in society are democratically run would serve as a check on whatever authoritarian or exploitative tendencies the owner might have. Such small businesses would in no way threaten the basic structure of Economic Democracy. In fact, they would provide added flexibility. Such small businesses can get their start-up capital from the investment banks. These banks, charged with providing investment funds to potentially profitable enterprises that will increase employment, will make funds available to promising small businesses, whatever their internal structure.

But small businesses don�t really address the entrepreneurial issue. Certainly, small businesses are often “entrepreneurial” in seizing specific opportunities—a new restaurant here, a new boutique there, a dollar-store on the corner—but such businesses contribute little in the way of technological improvement or new product design. The entrepreneurial talent that creates or exploits large technical or conceptual breakthroughs must be able to mobilize large amounts of both capital and labor. Being able to set up your own small business isn�t enough.

The basic model of Economic Democracy encourages communities to set up entrepreneurial agencies—institutions that research investment opportunities and provide technical advice and bank capital to those individuals interested in setting up new worker cooperatives. Society may want additional, complementary institutions to encourage entrepreneurial activity. Business schools, for example, could instruct students in the art of setting up successful cooperative enterprises. Local employment agencies could aid prospective entrepreneurs in recruiting workers. Financial incentives—bonuses and prizes—could be awarded to individuals who set up successful new cooperatives.

Such institutions may well be sufficient to keep the economy dynamic. The record of Mondragon is certainly impressive in this respect. There may well be enough people with entrepreneurial talent willing to exercise those talents in a democratic setting to maintain a healthy flow of new technologies and products. The citizenry of the nation may well be satisfied with the pace of change these “socialist entrepreneurs” would provide. (This pace may not be “maximal”—perhaps not as rapid as under certain periods of capitalism—but new and faster is not always better. Change that is too rapid can be unsettling and sometimes destructive of genuine values. Small is often beautiful. Speed can be an unhealthy addiction.)

An Economic Democracy that chooses a more measured rate of technological innovation than some of its more dynamic neighbors needn�t fear that “falling behind” would entail terrible consequences. Economic development need not be viewed as a race, wherein not to win is to lose. We can copy technological developments made elsewhere, if it seems appropriate to do so. We need not fear that our investment capital will flow to greener pastures, or that our workers will emigrate en masse.

However, we might want to encourage more entrepreneurial innovation by supplementing our basic institutions with some large-scale capitalism. If the basic institutions of Economic Democracy provide society with sufficient technological and product innovation, then there is no need for capitalist entrepreneurs. But if society should find the pace of innovation too slow, or if it just fancies the idea of those with entrepreneurial talent being given freer reign, then the prohibition on private ownership of means of production and wage labor could be relaxed. New enterprises could be privately owned. They too could seek funding from our public banks—and would be assured that they would not be discriminated against for being structured as capitalist firms. They could hire whatever workers they could attract. They could grow as large as market conditions permitted, without any legal limitations apart from our basic antitrust statutes. The owners could retain for themselves whatever profits the firm generates.

There is only one restriction. The owners are free at any time to sell their firms—but only to the state. The government will pay them the value of the firm�s accumulated assets (upon which it had been paying its capital assets tax), then turn the enterprise over to the employees to be run democratically. (If a firm is not sold, it is turned over to the employees at the death of the founder, the asset value being paid to the estate of the deceased.) In the event of multiple founders, each has the option of selling his share at any time to the state. The state would then receive his share of the firm�s profits, until, eventually, the other founders selling out or dying, majority ownership has passed into state hands, at which time the firm is democratized.

These capitalist-entrepreneurs pose no threat to the basic institutions of Economic Democracy. Their ability to treat their workers in an exploitative manner is sharply curtailed by the presence of widely available democratic employment alternatives. Their incomes are tied to their active, entrepreneurial activity, not to their mere ownership of productive assets, and so do not become a source of perpetual reward. Indeed, such capitalists perform two honorable societal functions: serving as sources of innovative ideas, and as incubators for additional democratic firms.

As we shall see, the real damage done by capitalists under capitalism is not done by individual entrepreneurs acting creatively but by their collective, nonentrepreneurial control of the investment process. Under Economic Democracy, even with entrepreneurial capitalists, this control remains securely in the hands of the democratically accountable deliberative bodies that oversee the distribution of the tax-generated investment fund.

Capitalist acts among consenting adults need not be prohibited under Economic Democracy.

Fair Trade, Not Free Trade

The structures of Economic Democracy described thus far pertain to a national economy. But, as everyone knows, we now live in a global economy. How would Economic Democracy fare in this “new world order”? Is Economic Democracy possible in one country or would it have to be implemented on a world scale to be effective? What should be the nature of the economic linkages between an Economic Democracy and other countries?

From an economic point of view, there is no reason to think that Economic Democracy would not be viable in one country. If other countries, however internally structured, do not react with military aggression or an economic blockade, a country structured along the lines of Economic Democracy should thrive. Of course, if the country was poor, it would be difficult to bring the foreign multinationals located in that country under democratic control—but even in such a case, some sort of peaceful accord might be possible. (Much would depend on the state of the counterproject internationally.) It would also be difficult to attract foreign investment, since investment would confer no control over an enterprise—but less reliance on private foreign capital may not be a bad thing, even for a poor country.

In a rich country, Economic Democracy could easily work. Its internal economy would remain efficient and dynamic, and it could continue to trade peacefully with other countries, capitalist or socialist. However, because of the way workplaces and the investment mechanism are structured under Economic Democracy, there would be significant differences in the nature of the economic transactions. Above all, there would be virtually no cross-border capital flows. Since firms are controlled by their own workers, they will not relocate abroad. Since funds for investment are publicly generated and are mandated by law to be reinvested domestically, capital will also stay at home. Capital doesn�t flow out of the country—apart from a presumably small flow of private savings looking for higher rates of return abroad. Capital doesn�t flow into the country either, for there are no stocks or businesses to buy. The capital assets of the country, apart from those owned by our domestic entrepreneurial capitalists, are collectively owned—and hence not for sale.

The elimination of cross-border capital flows has two exceedingly important positive effects.

- There is no downward pressure on workers� incomes coming from company threats to relocate to low-wage regions abroad.

- Countries cannot cite the need to attract capital as an excuse for lax environmental or labor regulations.

Significant as these effects are, cooperative labor and a publicly generated investment fund do not completely negate international wage competition or the incentives to be soft with environmental regulation. Free trade (i.e., trade regulated only by supply and demand) encourages such behavior. If trade is free, domestic goods produced by high-wage workers will not be as competitive as comparable imported goods produced by low-wage workers. A similar imbalance occurs with respect to environmental or labor restrictions. To insulate itself from such detrimental tendencies, while at the same time contributing toward a reduction in global poverty, Economic Democracy will adopt a policy of “fair trade,” not “free trade.” Free trade is fine so long as the trading partners are roughly equal in terms of worker incomes and environmental regulations. Such competition is healthy competition. However, when trading with a poorer country or one whose environmental or labor regulations are lax, Economic Democracy will adopt a policy of socialist protectionism.

“Protectionism” is, of course, a dirty word in mainstream discourse—despite the fact that virtually every economically successful nation of the capitalist era has been protectionist. We needn�t point to Japan. The record goes back much further. Alexander Hamilton, in his 1791 Report on Manufacturers, argued (successfully) that “the United States cannot exchange with Europe on equal terms, and the want of reciprocity would render them the victim of a system of reciprocity which would induce them to confine their views to Agriculture and refrain from Manufactures.”

Three-quarters of a century later, President Ulysses S. Grant observed:

For centuries England has relied on protection, has carried it to extremes and has obtained satisfactory results from it. There is no doubt that it is to this system that it owes its present strength. After two centuries, England had found it convenient to adopt free trade, because it thinks that protection can no longer afford it anything. Very well, Gentlemen, my knowledge of my country leads me to believe that within two hundred years, when America has gotten all it can out of protection, it too will adopt free trade.

In point of fact, a degree of protectionism can be good for a country, not only to allow for the development of local industries (the concern motivating Hamilton and Grant) but to prevent the sort of competition that puts downward pressure on domestic wages and on environmental regulations.

Economic Democracy�s fair trade policy is motivated by two distinct considerations. On the one hand, we want to protect our own workers from the sorts of competition that are damaging to everyone in the long run. On the other hand, we want to contribute positively toward alleviating global poverty. Both these goals can be met if trade policy is appropriately designed.

The socialist conviction underlying fair trade is the moral conviction that one should not, in general, profit from, or be hurt by, the cheap labor of others. To the extent that inequalities are necessary to motivate efficient production, they are justifiable. However, consumers should not benefit because workers in other countries work for lower wages than home-country workers, nor should home-country workers be put at risk by these lower wages. This conviction suggests the following two-part trade policy:

- A “social tariff” will be imposed on imported goods, designed to compensate for low wages and/or a lack of commitment to social goals regarding the environment, worker health, safety, or social welfare. (This is the protectionist part.)

- All tariff proceeds are rebated back to the countries of origin of the goods on which the tariffs were placed. (This is the socialist part.)

As a first approximation, the social tariff raises the price of an imported commodity to what it would be if workers in the exporting country were paid wages comparable to those at home and if environmental and other social expenses were the same. This figure would then be adjusted downward to compensate for the fact that poor-country workers may be using less productive technologies. (Unless some such adjustment is made, it will be almost impossible for poor-country manufacturing industries to compete with rich-country industries, since, given the relatively greater degree of labor intensity in most poor-country industries, a tariff that would equalize labor costs would make the poor-country goods much more expensive than that produced by a rich-country competitor.)

The point is to allow for competition, but only of a healthy sort. This “protectionist” trade policy derives from the stance Economic Democracy takes with regard to competition in general. Economic Democracy is a competitive market economy, but it discriminates between socially useful kinds of competition—those fostering efficient production and satisfaction of consumer desires—and socially destructive kinds of competition—those depressing wages and other social welfare provisions or encouraging lax environmental controls. Social tariffs are meant to block the latter without interfering with the former.

These social tariffs do more than shield domestic industries from socially undesirable forms of competition, for they are imposed on all imports from poor countries—foodstuffs and raw materials, as well as manufactured goods. Consumers will thus pay “fair prices” for goods imported from poor countries as opposed to the lower prices dictated by low wages abroad, whether or not these goods compete with those produced by local industries.

These social tariffs thus embody a socialist commitment to international labor solidarity. Income from these tariffs imposed on imported goods does not go into the general revenue fund of the importing country, but is sent back to the poor countries doing the exporting. Thus, with socialist protectionism, harmful competition is constrained, but the negative effect of the tariffs on poor countries is mitigated. Consumers in rich countries must pay “fair prices” for their imported goods—to protect their own workers from destructive wage competition, and to help alleviate global poverty. Because the consumers in Economic Democracy are paying higher prices for consumer goods, in part to help alleviate global poverty, the rebates should be directed to those agencies in the poor country most likely to be effective in addressing the problems of poverty and attendant environmental degradation—state agencies (where effective), labor unions, environmental groups, and other relevant nongovernmental organizations.

To be sure, these higher prices will likely decrease the consumption of imports from poor countries, which will adversely affect certain workers in those countries during the transition period. However, the overall effect of the higher prices accompanied by tariff rebates is to allow poor countries to devote fewer of their resources to producing for rich-country consumption, and thus to have more available for local use. The long-run consequences here are favorable to both rich nations and poor nations alike. (There is something obscene about poor countries using their best land and resources to satisfy the desires of rich-country consumers rather than the needs of their own people—as tends to be the case under capitalist free trade.)

To sum up briefly: Economic Democracy is a competitive market economy, but it is not a free-trade economy. It will engage in free trade with countries of comparable levels of development, but not with poorer countries. With a poor country, fair trade is better than free trade—for both countries.